Acquisitions

YIT increased its holding in YIT Moskovia by 5.92 percentage points and now holds all of the shares in the company. The purchase

price was EUR 5.1 million.

Demerger

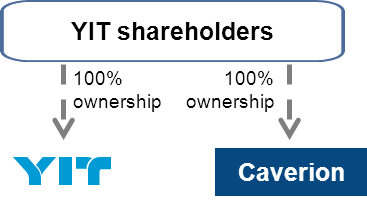

In 2013 conducted a partial demerger where YIT's Building Systems business was transferred to a company established in the demerger named Caverion Corporation.

Additional information

The implementation of the demerger was registered with the Finnish Trade Register on 30 June, 2013 and, therefore, all of the assets and liabilities related to YIT's Building Systems business were transferred to a company established in the demerger named Caverion Corporation (“Caverion”).

Following the implementation of the demerger, Caverion Corporation is an independent public limited company, separate from YIT Corporation. Before 30 June 2013, in YIT’s financial reporting, Caverion’s business was disclosed as a separate line item under discontinued operations with the exception of the balance sheet. The balance sheet was not adjusted in the official comparative information compliant with IFRS; rather, it also included the items associated with the Building Services business, thus corresponding to the previously reported balance sheet of YIT Corporation. Due to this, the balance sheet disclosed as comparative information does not, in this respect, illustrate the financial position of the continuing operations.

Further information about the resolutions passed at the Extraordinary General Meeting 17 Jun 2013

Materials

Registration Document and Demerger Note and Summary relating to the partial demerger

Registration document

Demerger Note and Summary

Supplement to Demerger Circular (27 Jun)

Supplement to Demerger Circular (1 Jul)

Marketing brochure relating to the partial demerger

Marketing brochure

Offer memoranda relating to the floating rate bond tender offer

Offer Memoranda

Demerger plan

Attachment to the Stock Exchange Release on 21 Feb

Report of Organisational Actions Affecting Basis of Securities in the USA

US Form 8937

Acquisition cost of YIT Corporation and Caverion Corporation

Read more about determination of acquisition costs of the shares for Finnish taxation purposes.